I am herewith reproducing the docuument sent by our dealer Mr. Rajiv, M/s Amar Jyothi Fuels, Hyderabad, who presented the same at Dealer Convention of SEC DO, 2011 regarding the Presentation by Dealer fraternity on changing scenarios of operations, marketing, technology in use at our Retail Outlets.

Presentation by Dealer fraternity on changing scenarios of operations, marketing, technology in use at our Retail Outlets.

28th March 2011

In 2000:

Dealer had very less paper work and used to spend very less time behind the desk.

Dealer had lot of time to interact with the customers.

Dealer had lot of time for marketing.

Now in 2011:

Dealer has lots of paper work and spends good amount of time behind the desk.

Dealer has very less time to interact with customers.

Dealer has very less time to do marketing.

In 2000:

Dealer had time to keep an eye on the day to day activities (House Keeping, sales men, customer grievances etc…) at the RO.

Dealer was happy with the profits with Limited Retail Outlets to compete.

Dealer had good profit in Lube Sales as the prices were low with good margin.

Now in 2011:

Dealer has no time left because manual data entry is required in spite of honeywell automation and also other activities like TT retention samples, etc…) apart from following all the old procedures.

Dealer started looking for new businesses for additional income to survive and even to compete with the New ROs which are mushrooming like weeds.

Profits vaporized from Lube Sales.

In 2000:

Maintenance of Approach Road, Driveway, Dispensing units was taken up on time by the company as the number of RO’s were less.

Adequate dispensing units for giving quick and quality service were provided.

With less investment and good financial help from the company like Cheque/DOD/5-day revolving credit facilities we could extend credit to the customers to attain good volumes.

Now in 2011:

Delay in Maintenance of Approach Road, Driveway, Dispensing units, etc…

With shortage of dispensing units and non availability of spares we are in no position to give good customer service.

As the fuel prices have gone up by more than 2 folds the investment increased and by withdrawing Cheque/DOD/5-day revolving credit facilities, we are in no position to extend the same to the customers due to which we are loosing volumes to other oil companies.

Result :

No personal interaction with the customers.

No new business developments.

Customer feels ignored.

No control over the staff.

Ultimately loss of sales.

Solution :

Streamlining the paper work with less redundancy.

Effective support and timely response from company officials.

Use of professional help for handling complaints and maintenance of RO.

More remuneration for hiring skilled & educated staff for providing better service.

Cheque / eDOD / 5-day revolving credit facility should be extended to performing dealers even in small towns and villages to improve the volumes.

2-Stroke engines replaced by 4-Stroke engines.

Regular shortage of some grades like KoolPlus, Brake Fluid, Futura, etc. is driving the customer away.

SSA & SSI entering the retail market and poaching our customers.

Diminishing of road-side workshops and authorised service centers not allowing oil purchased from us by threatening loss of warranty.

Good quality lubes and fine engines have extended lube changing cycle.

Proper availability of small packs of all the grades should be ensured.

Improvement is needed in sealing and packing of the product to gain customer confidence.

Strict action should be taken against SSA / SSI if they are making a direct sale to the end-user.

If maintenance of DU’s is not done periodically we noticed irregularities in product delivery, which in turn is creating a negative picture of the dealers.

As the facility to deliver the product in rupees was introduced to avoid the inconvenience of providing proper change to the customer the dealer is getting a dent in his profits as some of the DU manufactures have a display of only 2 decimals for quantity calculation due to which excess product is delivered when product is given in rupees.

The new policy for Xtracare has a criteria where the reimbursement is based on MS sales irrespective of the area (Urban / Rural). Where as the old policy was based on location of the RO and even the reimbursement and man power requirement were accordingly. But as per the new policy the man power requirement for all the RO’s is the same due to which the reimbursement given to a low MS selling outlet is not sufficient for maintenance. We kindly request you to rewrite the policy to suit every Xtracare RO taking into consideration all product sales as a rural RO has low MS and high HSD sales.

Most of the dealers have observed variation beyond permissible limits in underground tank stock when the product volume is low or vise versa. We request the company to take necessary action to avoid penal actions against the dealer.

We dealers have even observed no change in volume (dip levels) of the product in the TT even though there are high variations in the temperature from loading point to the receiving point.

We have been receiving product with different densities in a short span of days and because of this there are huge variations in density in our underground tank beyond permissible limits. We request you to attend to this issue and also provide a solution.

Cantonment and Tool charges are not reimbursed to the dealers for unknown reasons.

Most of the dealers have not received their security deposits given for previous TT contract.

Without proper guidelines, modifications to the TT at the time of calibration, non approved color scheme, branding, etc., which attracts additional expenditure should not be imposed.

The security deposit collected for reconstitution should be reduced and also waiver of security deposit should be given if it is done within the family.

Regular updates should be done in reconstitution policies as per legal requirements to avoid unnecessary delays.

In spite of having a company helpline to register dealer complaints no issue is attended in a proper timeline. We request you to have enhanced dealer friendly complaint logging facility to have escalation levels as well as web / tele enabled tracking system.

Thursday, March 31, 2011

Thursday, March 10, 2011

Service Tax on Goods Transport OperatorsUps and Down

INTRODUCTION:-

“Though no one can go back and make a brand new start, anyone can start from now and make a brand new ending….” But ending is not the fate of every start, some issues only have start and no end seems even after passing of no. of years – It is surely applicable on the service tax on goods transport operator services.

Service tax on transportation had a bad innings right from its first levy. It has gone through the ups and downs since it was levied for the first time on 16.11.1997. The levy was challenged and was withdrawn on 2.6.1998 just after few months. Though government did retrospective amendments twice in this category of service, yet the issue does not seem to be settled till date. The levy of service tax for the mid-period of 16.11.97 to 2.6.98 is still in limelight by one reason or another. Here is the anatomy of the issue that has been on fire since past so many years.

HISTORY:-

The history of service tax on transportation begins with Finance Act, 1997 which proposed the levy under the category of “Goods Transport Operator”. Notification no. 41/97, dated 5-11-1997 was issued in this regard which was effective from 16.11.1997. Clarifications regarding the levy were issued vide Circular F. No. B 43/11/97-TRU, dated 6-11-1997. But it was a bleak tax right from the beginning.

WHAT WAS THE UN-DIRECTIONAL PATH IN SERVICE TAX LEVY?

Notification No. 42/97-ST dated 5.11.1997 was issued which inserted Rule 2(1)(d)(xvii) of the Service Tax Rules, 1944 whereby the customer of the goods transport operator was made responsible for collecting the service tax. In other words, the liability to pay the service tax was shifted to the customer, i.e. the person who hires the service of transporter. This was unconventional method of taxation which was initiated by the government; as such it faced a lot of opposition from public. The transporters went on country-wide strike against this levy. Various petitions were filed for reversing the levy. The issue was settled (as it seemed then) by the hon’ble Supreme Court in the case of Laghu Udyog Bharti.

JUDGEMENT OF APEX COURT:-

The levy of service tax on goods transport operator's services was set at zilch by the Hon’ble Supreme Court in the case of M/s. Laghu Udyog Bharati V/s Union of India [1999 (112) E.L.T. 365 (S.C.)] who has held that the levy of tax from the receiver was illicit as the same is ultra vires the Finance Act, 1994. In this case, it was held that the levy of service tax on the recipient of the service instead of person providing the service was clearly illegal and unsustainable in law. It was further held that all the refund claims, if filed within time, are required to be finalized within 12 weeks from the date of filing. The amount duly worked out and verified should be effectively refunded to the claimant or the consumer welfare fund, as the case may be, within the period of 12 weeks as per the decision of Supreme Court rendered on July 27, 1998.

WITHDRAWN OF LEVY:-

In view of the aforesaid judgment of the Supreme Court, levy of the service tax on the services provided by the goods transport operator was exempted vide Notification No. 49/98-ST, dated 2.6.1998. As a consequence of this notification, various trade notices were issued which directed the field formations to drop the show cause notices issued under this levy. The recoveries were seized and the service tax already paid was directed to be refunded.

FINANCE ACT 2000:-

Finance Act, 2000 made amendments to the relevant provisions with retrospective effect. Amendment sought to validate levy and collection of service tax for the period between 16-7-1997 to 12-5-2000 in respect of services of goods transport operators. The amendment also sought to deny refund of service tax to users and also for recovery of refund already granted consequent to the judgment of the Supreme Court in Laghu Udyog Bharti. Recovery of refunds already granted was to be done within 30 days from the date when the Finance bill, 2000 received the assent of the President. In the event of non-payment of service tax so refunded by an assessee, the interest @ 24% p.a. was to be charged after the said period of 30 days.

Fresh show cause notices were issued to the appellant on different dates in 2002 demanding service tax from them for the services received from goods transport operators. Show cause notice proposed to invoke extended period of limitation and there was also a proposal for imposition of penalty and demand of interest. It is the case of the appellants that no show cause notice could have been issued to them under Section 73 even after the amendment brought under Finance Act, 2000.

BUDGET, 2003:-

The Government of India has come for a fresh dose of retrospective law with Budget 2003. This budget amended the section 68 retrospectively for making the customer of GTO as the person liable to pay the service tax. A new section 71A was inserted for making customer liable to furnish the service tax return within six months from the date on which the Finance Bill, 2003 received the assent of the President. Rule 7A was inserted according to which return was also to be furnished for the period from 16.11.97 to 2.6.98 within six months from 13.5.2003, failing which, all the consequences like interest and penalty were to be followed.

CONSEQUENCES OF RETROSPECTIVE AMENDMENTS:-

But inspite of all these retrospective amendments, there remained certain errors and the case bended on part of the assessees. The section governing the issue of show cause notice, i.e. section 73 left to be amended. The language of this section still had the language that the show cause notice can be issued if there is default in filing of return under section 70 and whereas the recipient of GTO services were to file the return under section 71A. This lacuna was followed by the no. of judgments. Further, the limitation clause also benefitted the assessees but it couldn’t stop the proceedings initiated by the department.

JUDICIAL PRONOUNCEMENTS:-

In case of L.H. SUGAR FACTORIES LTD. V/s COMMISSIONER OF C. EX., MEERUT-II [2004 (165) E.L.T. 161 (Tri. - Del.)], Tribunal passed the order rejecting the Show Cause Notices issued under section 73 for recovering the allotted refund as well as interest and penalty stating that since Appellant is required to submit the Return under section 71A then SCN cannot be issued u/s 73 as only be issued only the case of assessees who are liable to file return under Section 70.

In case of CCE, Vadodara-II V/S Welspun Gujarat Stahl Rohren Ltd. [200-TIOL-108-CESTAT-AHM], Tribunal held regarding Time Limitation of issuance of SCN relating to filing of Return by the recipients of the said service that the SCN must be issued within one year from the relevant date which was the 14/11/2003 i.e. date of insertion of section 71A in Finance Act through BUDGET 2003. The decision has been made relying upon the decision made in case of Mangalam Cement Ltd. as reported in [2007-TIOL-906-CESTAT-DEL]. From this decision one law point was cleared that SCN can be issued after one or two or three or so on years but should be within one year from new amendment in law itself relating to same matter.

OUTCOMES OF JUDICIAL PRONOUNCEMENTS:-

The decision of L.H. Sugar Factories Ltd was corrected by substituting the section 73. Finance (no. 2) Act, 2004 substituted this section w.e.f. 10.9.2004. After this amendment, the show cause notice can be issued on failure to file the return under section 70 as well as section 71A read with rule 7A of the Service Tax Rules, 1994.

But the conflicting decisions given on the issue of limitation resulted into reference to larger bench. The larger bench decided the reference in favour of the Revenue. This decision is cited as M/s Agauta Sugar & Chemicals Vs CCE, Noida [2010-TIOL-1185-CESTAT-DEL-LB] wherein it is held that show cause notice demanding the service tax for the period from 16.11.1997 to 1.6.1998 issued in 2004 after the amendment to Section 73 of the Finance Act, 1994 is valid. Thus, the larger bench struck off the expectations of the poor assessees. But this also did not ended the issue. Again a decision came in favour of the assessees during the last quarter of year 2010.

LATEST JUDGEMENT:-

The latest judgement in this sequence has been reported in 2010-TIOL-1208-CESTAT-AHM in case of CCE, VAPI V/S M/s. Mutual Industries Ltd. in which the CESTAT again dismissed the Appeal of Revenue. The view taken by the hon’ble Tribunal was that demand for the period from 16.07.1997 to 15.10.1998 was confirmed on the basis of retrospective amendments to pertinent provisions. In such a case, question of suppression of facts, fraud or collusion does not arise. So, SCN issued after one year but within 5 years is no more sustainable. So, even after the decision of larger bench, the issue is not yet settled.

BEFORE PARTING:-

In spite of all retrospective modifications have been made by the Government of India, they are not able to collect the service tax on “Goods Transport Operator” service for that numinous period between November, 1997 and June, 1998. One question is arising from all the recipients of the said service that why the department is so meticulous about collecting the tax for that tiny period? Will any further alteration of retrospective nature in law solve the matter absolutely? No one knows, but everyone is waiting to have this issue dumped forever.

COURTESY: SIMPLE TAX INDIA

“Though no one can go back and make a brand new start, anyone can start from now and make a brand new ending….” But ending is not the fate of every start, some issues only have start and no end seems even after passing of no. of years – It is surely applicable on the service tax on goods transport operator services.

Service tax on transportation had a bad innings right from its first levy. It has gone through the ups and downs since it was levied for the first time on 16.11.1997. The levy was challenged and was withdrawn on 2.6.1998 just after few months. Though government did retrospective amendments twice in this category of service, yet the issue does not seem to be settled till date. The levy of service tax for the mid-period of 16.11.97 to 2.6.98 is still in limelight by one reason or another. Here is the anatomy of the issue that has been on fire since past so many years.

HISTORY:-

The history of service tax on transportation begins with Finance Act, 1997 which proposed the levy under the category of “Goods Transport Operator”. Notification no. 41/97, dated 5-11-1997 was issued in this regard which was effective from 16.11.1997. Clarifications regarding the levy were issued vide Circular F. No. B 43/11/97-TRU, dated 6-11-1997. But it was a bleak tax right from the beginning.

WHAT WAS THE UN-DIRECTIONAL PATH IN SERVICE TAX LEVY?

Notification No. 42/97-ST dated 5.11.1997 was issued which inserted Rule 2(1)(d)(xvii) of the Service Tax Rules, 1944 whereby the customer of the goods transport operator was made responsible for collecting the service tax. In other words, the liability to pay the service tax was shifted to the customer, i.e. the person who hires the service of transporter. This was unconventional method of taxation which was initiated by the government; as such it faced a lot of opposition from public. The transporters went on country-wide strike against this levy. Various petitions were filed for reversing the levy. The issue was settled (as it seemed then) by the hon’ble Supreme Court in the case of Laghu Udyog Bharti.

JUDGEMENT OF APEX COURT:-

The levy of service tax on goods transport operator's services was set at zilch by the Hon’ble Supreme Court in the case of M/s. Laghu Udyog Bharati V/s Union of India [1999 (112) E.L.T. 365 (S.C.)] who has held that the levy of tax from the receiver was illicit as the same is ultra vires the Finance Act, 1994. In this case, it was held that the levy of service tax on the recipient of the service instead of person providing the service was clearly illegal and unsustainable in law. It was further held that all the refund claims, if filed within time, are required to be finalized within 12 weeks from the date of filing. The amount duly worked out and verified should be effectively refunded to the claimant or the consumer welfare fund, as the case may be, within the period of 12 weeks as per the decision of Supreme Court rendered on July 27, 1998.

WITHDRAWN OF LEVY:-

In view of the aforesaid judgment of the Supreme Court, levy of the service tax on the services provided by the goods transport operator was exempted vide Notification No. 49/98-ST, dated 2.6.1998. As a consequence of this notification, various trade notices were issued which directed the field formations to drop the show cause notices issued under this levy. The recoveries were seized and the service tax already paid was directed to be refunded.

FINANCE ACT 2000:-

Finance Act, 2000 made amendments to the relevant provisions with retrospective effect. Amendment sought to validate levy and collection of service tax for the period between 16-7-1997 to 12-5-2000 in respect of services of goods transport operators. The amendment also sought to deny refund of service tax to users and also for recovery of refund already granted consequent to the judgment of the Supreme Court in Laghu Udyog Bharti. Recovery of refunds already granted was to be done within 30 days from the date when the Finance bill, 2000 received the assent of the President. In the event of non-payment of service tax so refunded by an assessee, the interest @ 24% p.a. was to be charged after the said period of 30 days.

Fresh show cause notices were issued to the appellant on different dates in 2002 demanding service tax from them for the services received from goods transport operators. Show cause notice proposed to invoke extended period of limitation and there was also a proposal for imposition of penalty and demand of interest. It is the case of the appellants that no show cause notice could have been issued to them under Section 73 even after the amendment brought under Finance Act, 2000.

BUDGET, 2003:-

The Government of India has come for a fresh dose of retrospective law with Budget 2003. This budget amended the section 68 retrospectively for making the customer of GTO as the person liable to pay the service tax. A new section 71A was inserted for making customer liable to furnish the service tax return within six months from the date on which the Finance Bill, 2003 received the assent of the President. Rule 7A was inserted according to which return was also to be furnished for the period from 16.11.97 to 2.6.98 within six months from 13.5.2003, failing which, all the consequences like interest and penalty were to be followed.

CONSEQUENCES OF RETROSPECTIVE AMENDMENTS:-

But inspite of all these retrospective amendments, there remained certain errors and the case bended on part of the assessees. The section governing the issue of show cause notice, i.e. section 73 left to be amended. The language of this section still had the language that the show cause notice can be issued if there is default in filing of return under section 70 and whereas the recipient of GTO services were to file the return under section 71A. This lacuna was followed by the no. of judgments. Further, the limitation clause also benefitted the assessees but it couldn’t stop the proceedings initiated by the department.

JUDICIAL PRONOUNCEMENTS:-

In case of L.H. SUGAR FACTORIES LTD. V/s COMMISSIONER OF C. EX., MEERUT-II [2004 (165) E.L.T. 161 (Tri. - Del.)], Tribunal passed the order rejecting the Show Cause Notices issued under section 73 for recovering the allotted refund as well as interest and penalty stating that since Appellant is required to submit the Return under section 71A then SCN cannot be issued u/s 73 as only be issued only the case of assessees who are liable to file return under Section 70.

In case of CCE, Vadodara-II V/S Welspun Gujarat Stahl Rohren Ltd. [200-TIOL-108-CESTAT-AHM], Tribunal held regarding Time Limitation of issuance of SCN relating to filing of Return by the recipients of the said service that the SCN must be issued within one year from the relevant date which was the 14/11/2003 i.e. date of insertion of section 71A in Finance Act through BUDGET 2003. The decision has been made relying upon the decision made in case of Mangalam Cement Ltd. as reported in [2007-TIOL-906-CESTAT-DEL]. From this decision one law point was cleared that SCN can be issued after one or two or three or so on years but should be within one year from new amendment in law itself relating to same matter.

OUTCOMES OF JUDICIAL PRONOUNCEMENTS:-

The decision of L.H. Sugar Factories Ltd was corrected by substituting the section 73. Finance (no. 2) Act, 2004 substituted this section w.e.f. 10.9.2004. After this amendment, the show cause notice can be issued on failure to file the return under section 70 as well as section 71A read with rule 7A of the Service Tax Rules, 1994.

But the conflicting decisions given on the issue of limitation resulted into reference to larger bench. The larger bench decided the reference in favour of the Revenue. This decision is cited as M/s Agauta Sugar & Chemicals Vs CCE, Noida [2010-TIOL-1185-CESTAT-DEL-LB] wherein it is held that show cause notice demanding the service tax for the period from 16.11.1997 to 1.6.1998 issued in 2004 after the amendment to Section 73 of the Finance Act, 1994 is valid. Thus, the larger bench struck off the expectations of the poor assessees. But this also did not ended the issue. Again a decision came in favour of the assessees during the last quarter of year 2010.

LATEST JUDGEMENT:-

The latest judgement in this sequence has been reported in 2010-TIOL-1208-CESTAT-AHM in case of CCE, VAPI V/S M/s. Mutual Industries Ltd. in which the CESTAT again dismissed the Appeal of Revenue. The view taken by the hon’ble Tribunal was that demand for the period from 16.07.1997 to 15.10.1998 was confirmed on the basis of retrospective amendments to pertinent provisions. In such a case, question of suppression of facts, fraud or collusion does not arise. So, SCN issued after one year but within 5 years is no more sustainable. So, even after the decision of larger bench, the issue is not yet settled.

BEFORE PARTING:-

In spite of all retrospective modifications have been made by the Government of India, they are not able to collect the service tax on “Goods Transport Operator” service for that numinous period between November, 1997 and June, 1998. One question is arising from all the recipients of the said service that why the department is so meticulous about collecting the tax for that tiny period? Will any further alteration of retrospective nature in law solve the matter absolutely? No one knows, but everyone is waiting to have this issue dumped forever.

COURTESY: SIMPLE TAX INDIA

Wednesday, March 9, 2011

AP Minimum Wages Act for FY 2010-2011

Dear All,

Please download the AP minimum Wages act for the Petrol Pumps & TT Crew for the Financial Year 2010 - 2011. Copy and Paste the bottom link in the new tab for downloading the document!!!!

https://docs.google.com/viewer?a=v&pid=explorer&chrome=true&srcid=0B1POSkBAOcgcMmE1YjE2NTktNmJhNS00YTk5LTg2ZTEtZDdmZDZlYmY5YzE0&hl=en&authkey=CI6ojOcH

Source: Office of the Commissioner of Labour, Government of Andhra Pradesh

Disclaimer : Minimum Wages have been provided by the Labour Departments of respective states. All efforts have been made to update the minimum wage data on a regular basis. However, there might be unforeseen errors.

Please download the AP minimum Wages act for the Petrol Pumps & TT Crew for the Financial Year 2010 - 2011. Copy and Paste the bottom link in the new tab for downloading the document!!!!

https://docs.google.com/viewer?a=v&pid=explorer&chrome=true&srcid=0B1POSkBAOcgcMmE1YjE2NTktNmJhNS00YTk5LTg2ZTEtZDdmZDZlYmY5YzE0&hl=en&authkey=CI6ojOcH

Source: Office of the Commissioner of Labour, Government of Andhra Pradesh

Disclaimer : Minimum Wages have been provided by the Labour Departments of respective states. All efforts have been made to update the minimum wage data on a regular basis. However, there might be unforeseen errors.

Thursday, March 3, 2011

Tuesday, March 1, 2011

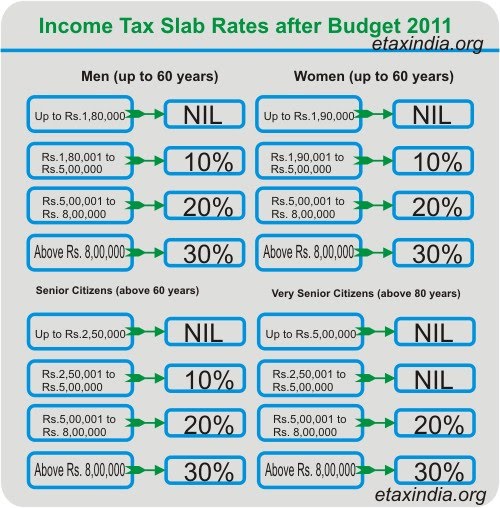

Union Budget 2011 Highlights on Tax

Union Budget 2011 Highlights on Tax

New category of senior citizens above 80 years to get higher IT deduction limit of Rs. 5 lakh from this year

Investment in fertiliser plants and machinery to be treated as infrastructure investment

IT exemption for taxpayers raised from Rs. 1.6 lakh to Rs. 1.8 lakh. Tax relief is about Rs. 2,000 across-the-board.

Govt to allow issue of Rs. 30,000 crore worth of tax-free bonds by infrastructure companies in 2011-12

Tax deduction for investment in infrastructure bonds of Rs. 20,000 extended for one more year Loss on direct tax reliefs at Rs. 11,500 crore; gain on indirect tax changes at Rs. 11,300 crore

Interest subvention on home loans up to Rs. 15 lakh. Mortgage risk guarantee corporation to insure loans to the poor

Cement excise duties will be shifted to valorem basis from specific duty now

Foreign individual investors allowed to invest directly in mutual funds subject to KYC requirements

Government considering extension of nutrient-based subsidy for urea, the largest chunk of fertilisers used in agriculture

Public sector disinvestment target for 2011-12 is raised to Rs. 40,000 crore

Corporate tax surcharge reduced from 7.5% to 5%. Minimum alternate tax rate up from 18% to 18.5%.

Fiscal deficit for 2010-11 seen at 5.1% against 5.5% budgeted; deficit for 2011-12 projected at 4.6% of GDP

FM says no need to remove stimulus package at this stage, but will withdraw excise exemptions

Senior citizens to get higher IT deduction limit of Rs. 2.5 lakh. Entitlement age reduced to 60 from current 65

Priority sector home loans limit raised to Rs. 25 lakh from Rs. 20 lakh.

Centre’s net borrowing figure for 2011-12 fixed at Rs. 3,43,000 crore; fiscal deficit figure at Rs. 4,12,000 crore

Government to introduce direct cash payments for those entitled to subsidies in kerosene, cooking gas and fertiliser by March, 2012.

Excise exemptions withdrawn on 130 items; to pay minimum excise of 1% from next year

Service tax levels and excise stay at 10%; Peak rate of customs duty remains unchanged

National mission for electric and hybrid vehicles to be set up to create environment-friendly automobiles

New category of senior citizens above 80 years to get higher IT deduction limit of Rs. 5 lakh from this year

Investment in fertiliser plants and machinery to be treated as infrastructure investment

IT exemption for taxpayers raised from Rs. 1.6 lakh to Rs. 1.8 lakh. Tax relief is about Rs. 2,000 across-the-board.

Govt to allow issue of Rs. 30,000 crore worth of tax-free bonds by infrastructure companies in 2011-12

Tax deduction for investment in infrastructure bonds of Rs. 20,000 extended for one more year Loss on direct tax reliefs at Rs. 11,500 crore; gain on indirect tax changes at Rs. 11,300 crore

Interest subvention on home loans up to Rs. 15 lakh. Mortgage risk guarantee corporation to insure loans to the poor

Cement excise duties will be shifted to valorem basis from specific duty now

Foreign individual investors allowed to invest directly in mutual funds subject to KYC requirements

Government considering extension of nutrient-based subsidy for urea, the largest chunk of fertilisers used in agriculture

Public sector disinvestment target for 2011-12 is raised to Rs. 40,000 crore

Corporate tax surcharge reduced from 7.5% to 5%. Minimum alternate tax rate up from 18% to 18.5%.

Fiscal deficit for 2010-11 seen at 5.1% against 5.5% budgeted; deficit for 2011-12 projected at 4.6% of GDP

FM says no need to remove stimulus package at this stage, but will withdraw excise exemptions

Senior citizens to get higher IT deduction limit of Rs. 2.5 lakh. Entitlement age reduced to 60 from current 65

Priority sector home loans limit raised to Rs. 25 lakh from Rs. 20 lakh.

Centre’s net borrowing figure for 2011-12 fixed at Rs. 3,43,000 crore; fiscal deficit figure at Rs. 4,12,000 crore

Government to introduce direct cash payments for those entitled to subsidies in kerosene, cooking gas and fertiliser by March, 2012.

Excise exemptions withdrawn on 130 items; to pay minimum excise of 1% from next year

Service tax levels and excise stay at 10%; Peak rate of customs duty remains unchanged

National mission for electric and hybrid vehicles to be set up to create environment-friendly automobiles

Union Budget 2011 Highlights on Tax

Union Budget 2011 Highlights on Tax

New category of senior citizens above 80 years to get higher IT deduction limit of Rs. 5 lakh from this year

Investment in fertiliser plants and machinery to be treated as infrastructure investment

IT exemption for taxpayers raised from Rs. 1.6 lakh to Rs. 1.8 lakh. Tax relief is about Rs. 2,000 across-the-board.

Govt to allow issue of Rs. 30,000 crore worth of tax-free bonds by infrastructure companies in 2011-12

Tax deduction for investment in infrastructure bonds of Rs. 20,000 extended for one more year Loss on direct tax reliefs at Rs. 11,500 crore; gain on indirect tax changes at Rs. 11,300 crore

Interest subvention on home loans up to Rs. 15 lakh. Mortgage risk guarantee corporation to insure loans to the poor

Cement excise duties will be shifted to valorem basis from specific duty now

Foreign individual investors allowed to invest directly in mutual funds subject to KYC requirements

Government considering extension of nutrient-based subsidy for urea, the largest chunk of fertilisers used in agriculture

Public sector disinvestment target for 2011-12 is raised to Rs. 40,000 crore

Corporate tax surcharge reduced from 7.5% to 5%. Minimum alternate tax rate up from 18% to 18.5%.

Fiscal deficit for 2010-11 seen at 5.1% against 5.5% budgeted; deficit for 2011-12 projected at 4.6% of GDP

FM says no need to remove stimulus package at this stage, but will withdraw excise exemptions

Senior citizens to get higher IT deduction limit of Rs. 2.5 lakh. Entitlement age reduced to 60 from current 65

Priority sector home loans limit raised to Rs. 25 lakh from Rs. 20 lakh.

Centre’s net borrowing figure for 2011-12 fixed at Rs. 3,43,000 crore; fiscal deficit figure at Rs. 4,12,000 crore

Government to introduce direct cash payments for those entitled to subsidies in kerosene, cooking gas and fertiliser by March, 2012.

Excise exemptions withdrawn on 130 items; to pay minimum excise of 1% from next year

Service tax levels and excise stay at 10%; Peak rate of customs duty remains unchanged

National mission for electric and hybrid vehicles to be set up to create environment-friendly automobiles

New category of senior citizens above 80 years to get higher IT deduction limit of Rs. 5 lakh from this year

Investment in fertiliser plants and machinery to be treated as infrastructure investment

IT exemption for taxpayers raised from Rs. 1.6 lakh to Rs. 1.8 lakh. Tax relief is about Rs. 2,000 across-the-board.

Govt to allow issue of Rs. 30,000 crore worth of tax-free bonds by infrastructure companies in 2011-12

Tax deduction for investment in infrastructure bonds of Rs. 20,000 extended for one more year Loss on direct tax reliefs at Rs. 11,500 crore; gain on indirect tax changes at Rs. 11,300 crore

Interest subvention on home loans up to Rs. 15 lakh. Mortgage risk guarantee corporation to insure loans to the poor

Cement excise duties will be shifted to valorem basis from specific duty now

Foreign individual investors allowed to invest directly in mutual funds subject to KYC requirements

Government considering extension of nutrient-based subsidy for urea, the largest chunk of fertilisers used in agriculture

Public sector disinvestment target for 2011-12 is raised to Rs. 40,000 crore

Corporate tax surcharge reduced from 7.5% to 5%. Minimum alternate tax rate up from 18% to 18.5%.

Fiscal deficit for 2010-11 seen at 5.1% against 5.5% budgeted; deficit for 2011-12 projected at 4.6% of GDP

FM says no need to remove stimulus package at this stage, but will withdraw excise exemptions

Senior citizens to get higher IT deduction limit of Rs. 2.5 lakh. Entitlement age reduced to 60 from current 65

Priority sector home loans limit raised to Rs. 25 lakh from Rs. 20 lakh.

Centre’s net borrowing figure for 2011-12 fixed at Rs. 3,43,000 crore; fiscal deficit figure at Rs. 4,12,000 crore

Government to introduce direct cash payments for those entitled to subsidies in kerosene, cooking gas and fertiliser by March, 2012.

Excise exemptions withdrawn on 130 items; to pay minimum excise of 1% from next year

Service tax levels and excise stay at 10%; Peak rate of customs duty remains unchanged

National mission for electric and hybrid vehicles to be set up to create environment-friendly automobiles

Direct cash subsidy on fuel, fertilizers by 2012

Seeking to address the issue of subsidies not reaching the targeted groups, Finance Minister Pranab Mukherjee on Monday proposed to provide a direct cash subsidy on fuel and fertilizers to the poor from March, 2012.

“To ensure greater cost efficiency and better delivery of kerosene and fertilizers, the government will move toward direct transfer of cash subsidy for people below poverty line (BPL) in a phased manner,” Mr. Mukherjee said during the presentation of the budget. The system would be in place by March, 2012, he added.

A task force headed by the former chief of Infosys, Nandan Nilekani, who is now Unique Identification Authority of India (UIDAI) Chairman, is working out the modalities for the proposed system, he said. It comprises Secretaries from the Ministries of Finance, Chemicals and Fertilizers, Agriculture, Food, Petroleum and Rural Development.

“The interim report of this task force is expected by June this year,” he remarked.

At present, the government provides kerosene at subsidised rates to BPL families through the Public Distribution System (PDS). Furthermore, LPG is provided at a subsidised rate to households. As regards fertilizers, the government provides subsidy to companies so that farm inputs, which include urea and imported fertilizers, can be provided to farmers at cheaper rates.

The need to set up the task force arose in view of overwhelming evidence that the current policy is resulting in waste, leakage, adulteration and inefficiency. Therefore, it is imperative that the system of delivering the subsidised kerosene be reformed urgently, the government said.

Besides designing an IT framework, the task force will align the systems with the issuance of the UID numbers and suggest changes in the administration and supply chain management. The recommendations of the task force will be implemented on a pilot basis by the Ministries concerned and the final report will include the results of such projects.

A new policy on providing subsidies on fertilizers on the basis of their nutrient composition could soon be extended to urea, one of the most widely used fertilizers, Mr. Mukherjee said. “Nutrient-based fertilizer policy for urea is under consideration.” The nutrient-based subsidy (NBS) regime is expected to promote balanced fertilization and consequently increase agriculture productivity in the country through higher usage of secondary and micro-nutrients.

“To ensure greater cost efficiency and better delivery of kerosene and fertilizers, the government will move toward direct transfer of cash subsidy for people below poverty line (BPL) in a phased manner,” Mr. Mukherjee said during the presentation of the budget. The system would be in place by March, 2012, he added.

A task force headed by the former chief of Infosys, Nandan Nilekani, who is now Unique Identification Authority of India (UIDAI) Chairman, is working out the modalities for the proposed system, he said. It comprises Secretaries from the Ministries of Finance, Chemicals and Fertilizers, Agriculture, Food, Petroleum and Rural Development.

“The interim report of this task force is expected by June this year,” he remarked.

At present, the government provides kerosene at subsidised rates to BPL families through the Public Distribution System (PDS). Furthermore, LPG is provided at a subsidised rate to households. As regards fertilizers, the government provides subsidy to companies so that farm inputs, which include urea and imported fertilizers, can be provided to farmers at cheaper rates.

The need to set up the task force arose in view of overwhelming evidence that the current policy is resulting in waste, leakage, adulteration and inefficiency. Therefore, it is imperative that the system of delivering the subsidised kerosene be reformed urgently, the government said.

Besides designing an IT framework, the task force will align the systems with the issuance of the UID numbers and suggest changes in the administration and supply chain management. The recommendations of the task force will be implemented on a pilot basis by the Ministries concerned and the final report will include the results of such projects.

A new policy on providing subsidies on fertilizers on the basis of their nutrient composition could soon be extended to urea, one of the most widely used fertilizers, Mr. Mukherjee said. “Nutrient-based fertilizer policy for urea is under consideration.” The nutrient-based subsidy (NBS) regime is expected to promote balanced fertilization and consequently increase agriculture productivity in the country through higher usage of secondary and micro-nutrients.

Subscribe to:

Posts (Atom)